{kind=link}

Nvidia and Amazon Internet Providers, the profitable cloud arm of Amazon, have a shocking quantity in widespread. For starters, their core companies emerged from a contented accident. For AWS, it was realizing that it might promote the interior companies — storage, compute and reminiscence — that it had created for itself in-house. For Nvidia, it was the truth that the GPU, created for gaming functions, was additionally properly suited to processing AI workloads.

That finally led to some explosively rising income in current quarters. Nvidia’s income has been rising at triple digits, transferring from $7.1 billion in Q1 2024 to $22.1 billion This fall 2024. That’s a reasonably superb trajectory, though the overwhelming majority of that development was within the firm’s knowledge heart enterprise.

Whereas Amazon by no means skilled that type of intense development spurt, it has constantly been a giant income driver for the e-commerce large, and each firms have skilled first market benefit. Over time, although, Microsoft and Google have joined the market creating the Huge Three cloud distributors, and it’s anticipated that different chip makers will finally start to achieve significant market share, too, even because the income pie continues to develop over the subsequent a number of years.

Each firms had been clearly in the suitable place on the proper time. As internet apps and cellular started rising round 2010, the cloud offered the on-demand sources. Enterprises quickly started to see the worth of transferring workloads or constructing purposes within the cloud, reasonably than working their very own knowledge facilities. Equally, as AI took off during the last decade, and enormous language fashions extra just lately, it coincided with the explosion in the usage of GPUs to course of these workloads.

Over time, AWS has grown right into a tremendously worthwhile enterprise, at the moment on a run fee near $100 billion, one which even separate from Amazon could be a extremely profitable firm. However AWS development has begun to decelerate, at the same time as Nvidia’s takes off. It’s partly the legislation of enormous numbers, one thing that may finally have an effect on Nvidia, too.

The query is whether or not Nvidia can maintain that development to turn out to be a long-term income powerhouse like AWS has turn out to be for Amazon. If the GPU market begins to tighten, Nvidia does produce other companies, however as this chart exhibits, these are a lot smaller income turbines which can be rising far more slowly than the GPU knowledge heart enterprise at the moment is.

Picture Credit: Nvidia

The short-term monetary outlook

Because the above chart notes, Nvida’s income development has been astronomical in current quarters. And based on each Nvidia and Wall Avenue analysts, it’s set to proceed.

In its current earnings report masking the fourth quarter of its fiscal 2024 (the three months ending January 31, 2024), Nvidia informed its buyers that it anticipates $24 billion value of income in its present quarter (Q1 FY25). In comparison with its year-ago first quarter, Nvidia expects to publish development of round 234%.

That’s merely not a quantity we frequently see from mature public firms. Nonetheless, given the corporate’s large income ramp in current quarters, its development fee is anticipated to say no. From a 22% income achieve from the third to fourth quarter of its just lately concluded fiscal 12 months, Nvidia anticipates a extra modest 8.6% development fee from the ultimate quarter of its fiscal 2024 to the primary of its fiscal 2025. Definitely, on a year-over-year comparability and never a glance again at simply three months, Nvidia’s development fee stays unbelievable for the present interval. However there are different development declines on the horizon.

For instance, analysts anticipate Nvidia to generate $110.5 billion value of income in its present fiscal 12 months, up simply over 81% from its year-ago outcomes. That’s dramatically decrease than the 126% achieve it posted in its just lately concluded fiscal 2024.

To which we ask: So what? For at the least the subsequent a number of quarters, Nvidia is anticipated to proceed scaling its income previous the $100 billion annual run fee mark, spectacular for a corporation that in its year-ago interval right this moment noticed whole revenues of simply $7.19 billion.

In brief, analysts, and to a extra modest diploma Nvidia, see enormous buckets of development forward for the corporate, even when a few of the eye-popping income development figures will gradual this calendar 12 months. It’s unclear what occurs on a barely longer timeframe.

Momentum forward

Plainly AI may very well be the reward that retains on giving for Nvidia for the subsequent a number of years, at the same time as extra competitors from AMD, Intel and different chipmakers begins to emerge. Very like AWS, Nvidia will face stiffer competitors finally, but it surely controls a lot of the market proper now, it will possibly afford to cede some.

Taking a look at it purely on the chip degree, not at boards or different adjacencies, IDC exhibits Nvidia firmly in management:

Picture Credit: IDC

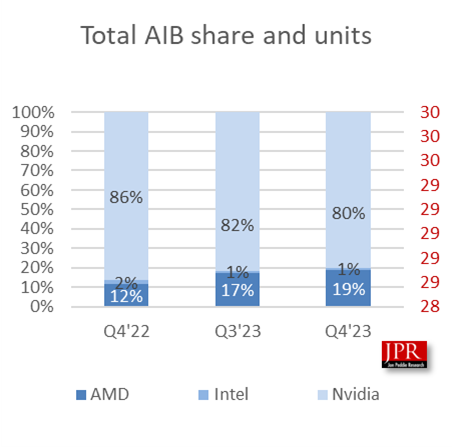

In the event you have a look at the board degree with these market share numbers from Jon Peddie Analysis (JPR), a agency that tracks the GPU market, whereas Nvidia nonetheless dominates, AMD is approaching stronger:

Picture Credit: Jon Peddie Analysis

C Robert Dow, an analyst at JPR, says a few of these fluctuations need to do with when new merchandise are launched. “AMD beneficial properties proportion factors right here and there relying on cycles available in the market — when new playing cards are launched — and stock ranges, however Nvidia has been in a dominant place for years, and that may proceed,” Dow informed TechCrunch.

Shane Rau, an IDC analyst who follows the silicon market, additionally expects the dominance to proceed, at the same time as traits shift and alter. “There are traits and countertrends, the markets during which Nvidia participates are huge and getting larger, and development will proceed, at the least for an additional 5 years,” Rau stated.

A part of the explanation for that’s Nvidia is promoting extra than simply the chip itself. “They’ll promote you boards, methods, software program, companies and time on certainly one of their very own supercomputers. So any of these markets are huge and rising and Nvidia is connected to all of them,” he stated.

However not everybody sees Nvidia as an unstoppable power. David Linthicum, a longtime cloud advisor and writer, says that you simply don’t at all times want GPUs, and firms are starting to comprehend that. “They are saying they want GPUs. I have a look at it, do a few of the again of the envelope math, and so they don’t want them. CPUs are completely high-quality,” he stated.

As this occurs, he thinks Nvidia will start to decelerate and competitors will loosen its stronghold in the marketplace. “I feel that we’re going to see Nvidia morph right into a weaker participant over the subsequent couple of years. And we’re going to see that as a result of there’s too many substitutes which can be being constructed on the market.”

Rau says different distributors can even profit as firms broaden AI use circumstances with Nvidia merchandise. “What I feel you’ll see going ahead is rising markets that’ll create tailwinds for Nvidia. However then there’ll be different firms that additionally comply with in these tailwinds that may profit from AI notably.”

It’s additionally doable that some disruptive power will come into play and that will be a constructive final result to maintain one firm from turning into too dominant. “You virtually hope disruption will occur as a result of that’s the best way markets and capitalism work finest, proper? Somebody will get an early lead, different suppliers comply with, the market grows. You get established gamers, who’re finally disrupted by a greater technique to do the identical factor inside their market or inside adjoining markets which can be crossing into theirs,” Rau stated.

The truth is, we’re starting to see that occuring at Amazon as Microsoft beneficial properties floor by way of its relationship with OpenAI and Amazon is compelled to play catch-up with regards to AI. No matter occurs to Nvidia in the long term, it’s firmly within the driver’s seat proper now, getting cash hand over fist, dominating a rising market and having nearly every little thing going its approach. However that doesn’t imply it can at all times be this fashion or that there gained’t be extra aggressive stress down the highway.